Let’s begin with defining the Reserves: Reserves are the amount of funds, time, or resources that are estimated from the risk management processes.

As per the PMBOK® Guide

As a further explanation, in a project, all the work performed as per project identified performance measurement baselines which include scope, schedule and cost baselines. In other words, work is performed for the identified scope with corresponding scheduling and cost of each item in the scope.

As every project results in a unique product, service or result, that’s why we need to consider the uncertainties involved in the project. These uncertain events may affect our ability to achieve project objectives, that’s why reserves are a mechanism to deal with cost and schedule risks.

There are two types of uncertainties involved in the project:

As per the PMBOK® Guide

Contingency Reserve:

The Budget inside the cost baseline or performance measurement baseline that is allocated for identified risks that are accepted and for which contingent or mitigating responses are developed.

Management Reserve:

The project budget amount kept for management objectives. These are budgets reserved for unforeseen work that is inside the scope of the project.

The management reserve is not included in the performance measurement baseline (PMB).

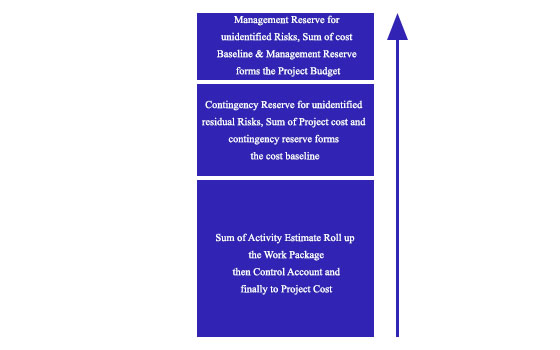

Below mentioned diagram shows difference between contingency and management reserve in the context of performance measurement baseline:

Difference between Contingency and Management Reserves:

| Contingency Reserves | Management Reserves |

|---|---|

| Designed to deal with Known – Unknown uncertainties | Designed to deal with Unknown-Unknown uncertainties. |

| Developed for the accepted risks remains after applying mitigation, risk response strategies; these are residual risks in the risk register. | Developed for unforeseen events and these are not mentioned in the risk register |

| Contingency reserves are included in the performance measurement baseline | Management reserves are not included in the performance measurement baseline. |

| These reserves are used when residual and/or an accepted risk occurs. | Management reserves are used when unforeseen events occur. The amount of time and cost used to account unforeseen work is added to the project performance baseline. |

| When we move towards project execution, more specific information about the project become available and these reserves may get reduced or eliminated. When accepted risks occur, these reserves are used. | When we move towards project execution these reserves are used when unforeseen risks occurs. |

| The project manager has complete authority about the usage of these reserves | A formal approval from project sponsor may be required for the usage of management reserve |

As to recollect:

Contingency Reserve is a cushion for the remaining risks which ensures that if they become reality this reserve should be able to absorb the impact and project team still can deliver in baseline time and duration.

As these are included in the performance measurement baseline, the project manager has authority on their usage. These reserves are used for already identified events and based on availability of precise information as project move through execution; these reserves may be used, reduced or eliminated.

Management Reserve is a kind of reserve to fund unforeseen events, as these are not included performance measurement baseline, their usage may require the involvement of the project sponsor.

Management reserves are included in the project budget and the amount depends on various factors like the ability to recognize customer nature, the complexity of the project etc. Historical records play significant role in designing management reserves. If you are developing the type of product first, time you may need more reserve. In most of cases a certain percentage of the total identified project cost is allocated as management reserves like 5% of total project cost, again it depends on various above mentioned factors.

I hope this blog has sufficiently answered your all queries related to what are Contingency Reserves and Management Reserves and the basic differences underlying them. You can post follow up questions here on our DISCUSSION FORUM. You may also want to check our other blogs PMP® Trainings.

Enroll to our FREE PMP® Certification Introductory Program to learn more about PMP® certification

No Trainings found